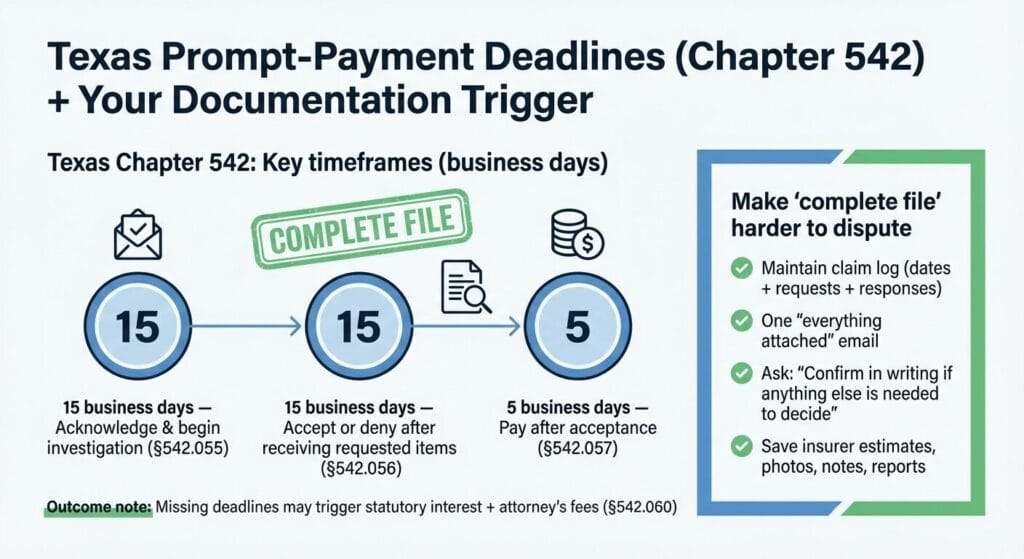

Texas Insurance Code Chapter 542 imposes some of the most unforgiving claims payment deadlines in the country. An insurer that misses any one of three statutory deadlines — 15 business days to acknowledge a claim, 15 business days to accept or deny after receiving all requested information, or five business days to pay after accepting — faces automatic penalty interest of 18 percent per annum plus attorney's fees. There is no discretion, no de minimis exception, and no cure period.

Enforcement of these requirements has increased heading into 2026, according to practitioners tracking claims litigation. The increase reflects both growing policyholder awareness of the prompt payment statute and a plaintiffs' bar that has become increasingly efficient at documenting missed deadlines in property and casualty claims.

Where Carriers Are Getting It Wrong

The most common source of prompt payment violations is not bad faith. It is process failure — specifically, the failure to track and document the dates that trigger each statutory deadline.

The 15-day acknowledgment clock starts when the insurer receives notice of the claim. For insurers receiving claims through multiple channels — phone, mail, agent, online portal — the question of when the clock started is frequently contested. If the insurer cannot produce a contemporaneous record showing when it received the claim, it cannot reliably demonstrate that its acknowledgment was timely.

The 15-day acceptance or denial clock starts when the insurer receives all items, statements, and forms requested from the policyholder. Carriers frequently extend this period by requesting additional documentation — but the request must be specific, and the clock restarts only for the items actually requested. A vague request for "additional information" does not toll the deadline indefinitely.

The five-day payment clock after acceptance is the most straightforward — and the one that most frequently generates violations in electronically administered claims. Payment system delays, authorization queues, and batch processing cycles can push the actual payment date past the statutory deadline even when the claim was accepted on time.

Third-Party Administrators and Prompt Payment

TPAs administering claims on behalf of insurers face prompt payment obligations under the insurer's license. A TPA that misses the deadline due to its own processing failures creates liability for the carrier — and the carrier's exposure is the same regardless of whether the delay was the insurer's fault or the TPA's.

Carrier contracts with TPAs increasingly include specific prompt payment performance standards and indemnification provisions for Chapter 542 violations. Carriers that have not reviewed their TPA contracts through a prompt payment lens should do so, particularly if their TPA is handling high-volume property claims where deadline tracking is most demanding.

What the Automatic Penalty Looks Like

On a $500,000 property claim that is paid 30 days late, the 18 percent annual penalty interest accrues at approximately $246 per day. A 30-day delay generates roughly $7,400 in penalty interest — plus the carrier's share of the policyholder's attorney's fees for pursuing the claim. On large commercial claims, the economics of prompt payment violations can dwarf the costs of the process improvements that would prevent them.

This article is for informational purposes and does not constitute legal advice.