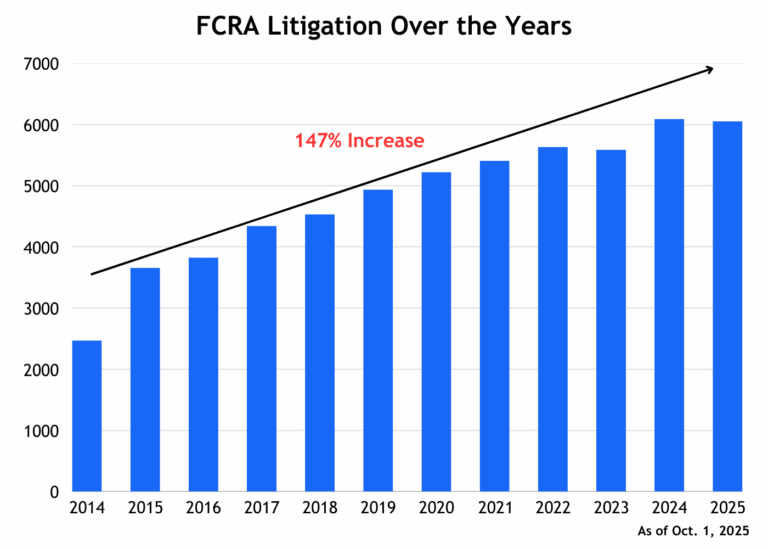

The numbers from January 2026 make a straightforward case about the current state of FCRA compliance risk. Lawsuit filings under the Fair Credit Reporting Act increased 47.5 percent compared to January 2025, according to litigation tracking data published by ACA International. FDCPA filings rose 26.5 percent over the same period. CFPB complaints climbed 26 percent.

Those increases happened while the Consumer Financial Protection Bureau was cutting its examination program to roughly 60 percent of its 2024 volume. The agency conducted 107 examinations in 2024. Its restructuring plan projects 64 examinations for 2026 — a reduction of more than a third.

The divergence between declining regulatory activity and rising litigation is not coincidental. It is structural.

Why Federal Pullback Doesn't Reduce FCRA Risk

The FCRA's private right of action — codified at 15 U.S.C. § 1681n and § 1681o — does not require a federal agency to file a complaint, issue guidance, or open an investigation. Consumers can sue directly, and plaintiffs' attorneys have built a sophisticated litigation industry around FCRA claims over the past decade. That industry does not depend on CFPB enforcement priorities to operate.

What the CFPB's withdrawal has done, according to practitioners, is shift the informational environment. The bureau has withdrawn virtually all of the advisory opinions and interpretive guidance it published over the past decade on FCRA compliance topics, including background screening. Furnishers and CRAs who relied on that guidance now face compliance questions that must be resolved by reading the statute, reviewing FTC materials, and watching litigation outcomes.

The CFPB also issued a new interpretive rule in late 2025 significantly expanding the scope of federal FCRA preemption. Under the new interpretation, states have considerably less room to impose additional consumer reporting protections than the bureau's 2022 guidance had recognized. That shift is expected to generate litigation over whether specific state laws — particularly medical debt reporting restrictions and criminal history reporting requirements — survive under the broader preemption standard.

The Class Action Dimension

Individual FCRA claims are significant. Class actions are existential. A furnisher or CRA whose standard procedure has a systemic flaw — a template response that does not constitute a reasonable reinvestigation, an automated dispute processing system that strips dispute content before routing — faces class action exposure that scales with every consumer affected by the practice.

The January 2026 litigation data reflects both individual and class filings. Even a fraction of that increase attributable to class actions represents disproportionate financial exposure compared to individual claim counts.

Furnishers reviewing their dispute investigation procedures should assume that plaintiff-side counsel is reading the same FCRA litigation data they are — and that the increase in filings reflects organized effort, not random variation.

This article is for informational purposes and does not constitute legal advice.